Next: Conditional finite-time yield dynamics

Up: Properties of the term

Previous: Instantaneous covariances

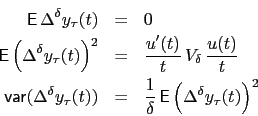

With the process for the zero-rates given in (![[*]](crossref.png) ), the integration

can be carried out to obtain the finite-time differences:

), the integration

can be carried out to obtain the finite-time differences:

|

(16) |

Unconditional expectation and variance are

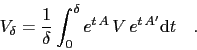

The finite-time covariance  is given in section

as

is given in section

as

|

(17) |

Markus Mayer

2009-06-22