Next: Diagonalisation of and

Up: EFM(2)

Previous: Introduction

The Economic Factor Model in its second specifation, EFM(2), is defined under objective measure  -dynamics as follows:

-dynamics as follows:

where  is a 3-d BM entering through full covariance

is a 3-d BM entering through full covariance

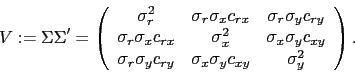

|

(45) |

Let

and introduce

and introduce

which gives the -SDE

|

(46) |

Specify the risk premium

|

(47) |

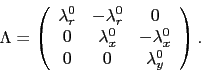

with matrix  given as

given as

|

(48) |

Under the risk-neutral measure  the dynamics reads

the dynamics reads

where

.

By introduciong new parameters the SDE can now be brought into the following -form

.

By introduciong new parameters the SDE can now be brought into the following -form

|

(51) |

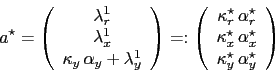

where

and

and

, i.e.

, i.e.

|

(52) |

and

|

(53) |

i.e. with this particular affine choice of  the structure of the dynamics is maintained

under risk neutral measure .

the structure of the dynamics is maintained

under risk neutral measure .

Next: Diagonalisation of and

Up: EFM(2)

Previous: Introduction

Markus Mayer

2009-06-22