Next:

Finite time portfolio evolution

Up:

Bond portfolios

Previous:

Bond portfolios

Local efficient frontier

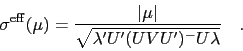

Since

the locally efficient portfolio is

(28)

and the efficient frontier is

(29)

i.e.

(30)

Markus Mayer 2009-06-22