Welcome to Tech - Science - Finance

A blog by Markus C. Mayer

Fixed Income Know-How

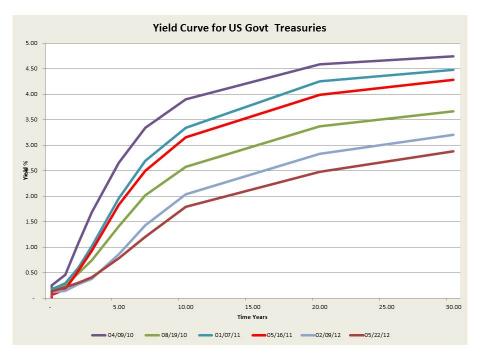

This is an introduction to the basic notions, conventions and applications of the term structure of interest rates, commonly called the yield curve. Here you will find a discussion of the basic notions like interest rate, discount factor zero, par ... Read more »

Hidden Markov Models

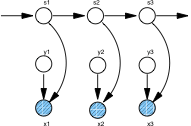

Hidden Markov models (HMMs) are briefly introduced and the major results are collected: Maximum likelihood inference, the Baum-Welch algorithm, and Monte-Carlo approaches. The document also contains an overview of selected HMMs that are of particular practical use. Click here. ... Read more »

The Economic Factor Model and a class of affine term structure models

The economic factor model is an affine term structure model where the factors have a particular economic interpretation. The general affine n-factor term structure model is presented and the EFM as a special case is developed in detail. The results ... Read more »