Statistics

The Kelly criterion and fixed fraction betting

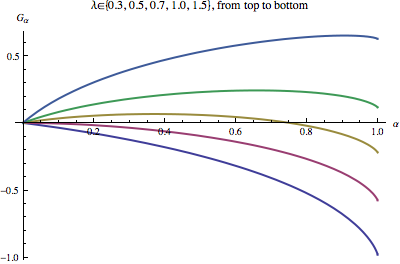

The Kelly criterion and fixed fraction betting is briefly introduced and extended to left bounded profit/loss distributions (i.e. profit/loss distributions that are bounded from the left). Various inequalities are studied and analytical tools are offered. Click here for the full text. Introduction### Let $X$ be a real