Next: Analytical solutions for

Up: kelly

Previous: kelly

Let  be a real random variable with support

be a real random variable with support

. Following Kelly [1] consider the reinvested growth of a fixed fraction investment in an instrument that has payoff

.

. Following Kelly [1] consider the reinvested growth of a fixed fraction investment in an instrument that has payoff

.

(If the support of

is bounded the restriction on  can be relaxed.)

The long run growth rate is

can be relaxed.)

The long run growth rate is

By the law of large numbers

|

(1) |

For a given

the function  is concave in

, and, writing

is concave in

, and, writing

we have

we have

.

Define the maximal growth rate as

.

Define the maximal growth rate as

![$\displaystyle G[X] = \max_\alpha\,{\mathsf{E}}\log(1+\alpha\,X)\quad.$](img15.png) |

(2) |

![$ G[X]$](img16.png) and

and

:

:

Since the slope of  at

at  , i.e.

, determines the location of the maximum we have, for

, i.e.

, determines the location of the maximum we have, for

![$ \alpha\in[0,1]$](img20.png) ,

,

Upper bound for

:

Jensen's inequality yields

and because of

and because of  and

and

it is

it is

![$\displaystyle G[X] \leq \log(1+{\mathsf{E}}X) \leq {\mathsf{E}}X \quad .$](img29.png) |

(5) |

Mixtures:

Consider a mixture

. We have

. We have

hence

![$\displaystyle G[X] \leq \max_Y G[X\vert Y] \quad ,$](img36.png) |

(6) |

i.e. the gain of a mixture cannot be larger than the gain of the best variable in the mixture.

Gambles that are offered with lower fequency  :

:

Suppose a gamble is offered at a reduced rate, i.e. at every step with probability

the payoff

is available and with probability  no investment is offered, i.e. the payoff is 0

. The pdf for payoff

no investment is offered, i.e. the payoff is 0

. The pdf for payoff  is

is

. Then

. Then

![$ \max_\alpha\widetilde{\mathsf{E}}\log(1+\alpha X) = \max_\alpha\left[\rho{\mathsf{E}}\log(1+\alpha X) + (1-\rho)\log(1)\right] = \rho G[X]$](img41.png) . Denoting the reduced rate gain, i.e. the maximal gain under

. Denoting the reduced rate gain, i.e. the maximal gain under

, as

, as ![$ G^\rho[X]$](img43.png) , it is

, it is

![$\displaystyle G^\rho[X] = \rho\, G[X] \quad .$](img44.png) |

(7) |

When several gambles

are offered with occurrence probabilities

are offered with occurrence probabilities

the individual gains are

the individual gains are

![$ \rho_iG[X_i]$](img47.png) . Amongst the offered gambles the one with largest

is favourable.

. Amongst the offered gambles the one with largest

is favourable.

Small edge

:

:

For small

we expand around

and the quadratic approximation gives

and then

and then

![$\displaystyle G[X] = \frac{1}{2} \frac{({\mathsf{E}}X)^2}{{\mathsf{E}}X^2},\quad \mathrm{for\ } {\mathsf{E}}X\rightarrow 0$](img51.png) |

(8) |

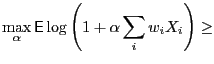

Gain of averages

:

:

A lower bound to

![$ G[\sum_i w_i X_i]$](img53.png) with

with

can easily be found:

can easily be found:

By convexity of the  function it is

function it is

![$ \max_\alpha\sum_i w_i\,G_i(\alpha) \geq\sum_i w_i\, \max_\alpha G_i(\alpha) = \sum_i w_i G[X_i]$](img60.png) , so we have

, so we have

![$\displaystyle G\left[\sum_i w_i X_i\right] \geq \sum_i w_i G[X_i] \geq \min_i G[X_i] \quad$](img61.png) |

(9) |

i.e. the gain of an average of payoffs is not smaller than the smallest gain.

Representation in terms of the cumulative distribution function:

Partial integration of the integral

results in a useful

representation for

. Denote the cdf

results in a useful

representation for

. Denote the cdf

.

Starting with

.

Starting with

partial integration gives (use

partial integration gives (use

)

)

observe that both terms separately diverge with

. To alleviate this problem

use

. To alleviate this problem

use

,

,

and after rearranging and letting

we have the desired result

|

(10) |

Representation in terms of the Laplace transform:

We will need a result for the Laplace transform of a (positive) random variable

,

. Doing partial integration of

. Doing partial integration of

analogous to the partial integration leading to

eq. (10) gives the following result that expresses the Laplace transform in terms of the cdf:

analogous to the partial integration leading to

eq. (10) gives the following result that expresses the Laplace transform in terms of the cdf:

|

(11) |

Starting with the shifted version of the cdf representation eq. (10)

and using

we get

and we can express the integral

via eq. (11) in terms of the cdf

via eq. (11) in terms of the cdf  to

obtain

to

obtain

|

(12) |

The restriction  in the equation above is used as a reminder that the relation holds

for the unshifted, i.e. positive random variable

.

in the equation above is used as a reminder that the relation holds

for the unshifted, i.e. positive random variable

.

It is tempting to use

to derive a relation, but issues with uniform continuity arise.

to derive a relation, but issues with uniform continuity arise.

Next: Analytical solutions for

Up: kelly

Previous: kelly

Markus Mayer

2010-06-04

![$\displaystyle \max_\alpha{\mathsf{E}}_X\log(1+\alpha X) = \max_\alpha{\mathsf{E...

...mathsf{E}}_{X\vert Y}

\underbrace{\log(1+\alpha X\vert Y)}_{\leq G[X\vert Y]} =$](img33.png)

![$\displaystyle G\left[\sum_i w_i X_i\right]$](img55.png)

![$\displaystyle G_\alpha^M = \Phi(M)\left[\int_{-1}^M\frac{\alpha}{1+\alpha x} dx+\log(1-\alpha)\right] - \int_{-1}^M \frac{\alpha\,\Phi(x)} {1+\alpha x}\, dx$](img69.png)